Do You Know How India’s Digital Payments Are Outpacing Cash Transactions

Explore how India’s digital payments, led by UPI, are surpassing cash transactions, transforming the economy, and shaping the future of finance.

BUSINESS & ECONOMY

Do You Know Team

9/27/20258 min read

India’s financial ecosystem has experienced one of the most remarkable transformations of the 21st century, moving rapidly from a predominantly cash-driven economy to a digital-first environment. For decades, cash remained the cornerstone of financial transactions, whether in bustling urban markets or remote rural villages. The physicality of cash, combined with limited banking penetration, meant that financial inclusion was uneven, and informal economies thrived. However, the advent of digital payments has disrupted this traditional model, creating a landscape where money moves seamlessly, securely, and almost instantaneously. This transition has been fueled by multiple factors: technological advancements, government initiatives, the rise of fintech startups, and a gradual shift in consumer behavior. Central to this change is the Unified Payments Interface (UPI), introduced in 2016, which has redefined how Indians transact. Today, UPI facilitates billions of transactions monthly, dwarfing traditional cash usage and reshaping the economic fabric of the nation. Beyond convenience, this shift represents a larger societal change—toward financial transparency, inclusion, and a modern economy capable of competing on a global scale.

The narrative of India’s digital payment revolution is as much about technology as it is about human behavior, societal adaptation, and economic restructuring. To understand how digital payments are outpacing cash, one must explore the interplay of historical trends, consumer psychology, technological adoption, government policy, and global benchmarks.

The Historical Context of Cash in India

For centuries, cash was more than just a medium of exchange in India; it was a symbol of trust and immediacy. Coins and banknotes were tangible proof of value, easily understandable by all layers of society. Early 20th-century India had informal money lending systems, barter trade in villages, and rudimentary banking that served only the urban elite. Even after independence, while banks and formal financial institutions proliferated, cash remained dominant due to its ease of use and the absence of alternative mechanisms.

With urbanization and economic reforms post-1991, India experienced rapid growth, and cash transactions continued to dominate retail, wholesale, and service sectors. Credit and debit cards emerged in metropolitan cities, yet adoption was slow. Most Indians preferred the certainty of cash over the perceived risks of digital banking. In rural areas, where literacy and infrastructure were limited, cash remained the only feasible medium of exchange, contributing to the persistence of informal economies.

It was only in the late 2000s that early digital innovations began to make inroads. Net banking allowed urban users to transfer money without visiting branches, and prepaid wallets provided an initial taste of digital convenience. However, these were fragmented solutions, limited in scope, and often inaccessible to the majority of the population.

The Technological Revolution and Digital Adoption

The proliferation of smartphones and mobile internet marked a turning point in India’s financial landscape. By 2025, India has over 750 million internet users, with mobile devices serving as the primary gateway to digital services. This connectivity enabled fintech startups to design user-friendly applications that cater to diverse demographics, including first-time users in Tier 2 and Tier 3 cities.

UPI emerged as the linchpin of this transformation. Unlike earlier platforms, UPI is interoperable across banks and apps, provides real-time settlement, and requires minimal technical know-how for users. Its integration with QR codes and mobile banking apps has made transactions as simple as scanning a code or entering a virtual ID, removing barriers that once hindered digital adoption.

Fintech innovations have complemented UPI, offering features like automated bill payments, recurring transfers, and integration with e-commerce platforms. AI-powered fraud detection systems and biometric authentication have enhanced security, fostering user trust. Consequently, digital payments have transitioned from a niche convenience to a preferred medium of exchange.

Government Initiatives: Driving the Digital Wave

The Indian government has played a pivotal role in promoting a cashless economy. Programs like Digital India, launched in 2015, sought to expand digital infrastructure and literacy. The Jan Dhan Yojana (PMJDY) brought millions of previously unbanked citizens into the formal banking system, enabling them to access digital payment platforms.

GST implementation further incentivized digital payments. Businesses that adopted electronic payment mechanisms found it easier to comply with tax regulations, maintain transparent records, and manage inventory efficiently. Government schemes such as PMGDISHA have taught citizens in rural areas how to use smartphones and digital tools, effectively democratizing access to digital financial services.

Moreover, policy measures by the Reserve Bank of India, including risk-based authentication guidelines, have increased the security and credibility of digital payments. By combining technology with regulatory oversight, the government has created an environment conducive to rapid digital adoption.

Consumer Behavior and the Shift from Cash

Consumer behavior has shifted dramatically in response to technological convenience, societal influence, and experiential learning. Millennials and Gen Z, comfortable with digital interfaces, prefer contactless and instantaneous payments over cash. The COVID-19 pandemic accelerated this trend, as safety and hygiene concerns prompted widespread adoption of digital payments.

Festive seasons highlight these behavioral patterns. During Navratri 2025, digital transactions spiked to ₹11.31 lakh crore in a single day, nearly a tenfold increase from the previous day. Consumers leveraged UPI, wallets, and mobile banking to make purchases quickly, avoiding the inconvenience of carrying large sums of cash. This surge demonstrates how behavior, trust in technology, and societal acceptance converge to drive adoption.

Behavioral psychology explains these shifts. Humans are wired for convenience, social proof, and incentives. Digital payments cater to these preferences by offering speed, security, cashback rewards, loyalty points, and social recognition through transaction confirmations and app notifications. This creates positive reinforcement loops, accelerating the replacement of cash.

The Decline of Cash Transactions

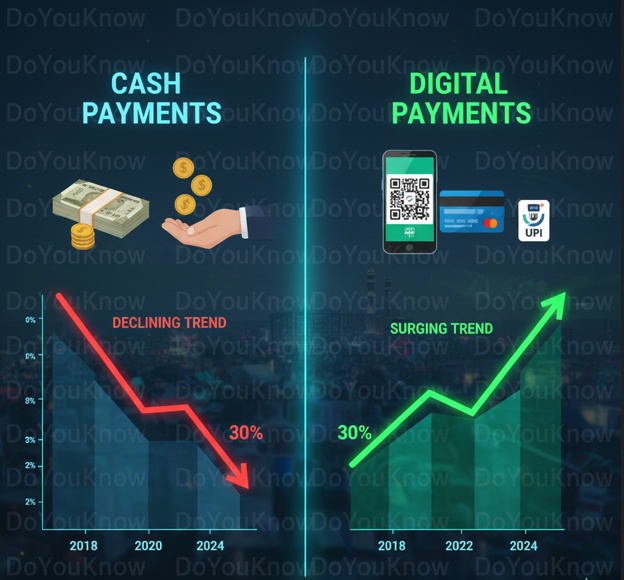

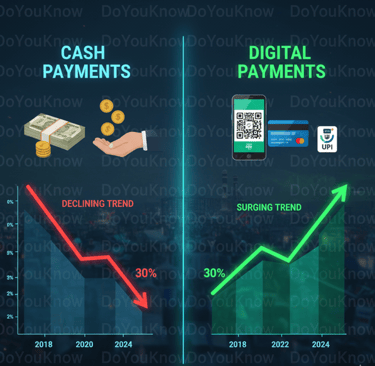

India’s cash economy, long dominant, is steadily declining. Currency in circulation relative to GDP has decreased, ATM withdrawals are plateauing, and merchants are increasingly incentivized to accept digital payments. By 2024, cash accounted for less than 60% of consumer spending, down from nearly 80% in 2021.

Businesses, particularly SMEs, have embraced digital payments to streamline operations, reduce handling costs, and attract a growing segment of digital-first consumers. E-commerce and retail companies report increased efficiency and reduced errors when transitioning to cashless systems. Consumers, in turn, appreciate transparency and convenience, further perpetuating the shift.

UPI: Transforming India’s Financial Landscape

UPI has become the cornerstone of India’s digital payments revolution. Since its launch in 2016, UPI has grown exponentially, processing billions of transactions monthly across multiple platforms. Its interoperability across banks ensures users are not locked into a single ecosystem. Features such as UPI AutoPay for recurring payments, instant merchant settlements, and integration with financial apps have expanded its utility far beyond peer-to-peer transfers.

The system’s scalability, reliability, and simplicity have set a global benchmark. India’s digital payments model has drawn interest from other countries, and discussions are underway to facilitate cross-border UPI transactions, positioning India as a leader in digital finance innovation.

Challenges in Digital Payments Adoption

Despite the remarkable growth, challenges remain. Security concerns are paramount. Fraudulent transactions, phishing, and cyberattacks necessitate robust authentication protocols, AI monitoring, and user awareness campaigns.

Infrastructure disparities also affect adoption. Rural and remote areas often face connectivity issues, and digital literacy gaps can hinder seamless usage. Government programs addressing these challenges are crucial to ensure that digital payments remain inclusive.

Regulatory frameworks must continuously evolve to balance innovation with security. The RBI’s proactive guidelines, including risk-based authentication, demonstrate how adaptive governance supports sustainable growth in the digital payments ecosystem.

Economic and Societal Implications

The shift from cash to digital payments has profound economic implications. Financial inclusion has improved as more citizens gain access to banking and digital financial services. The formalization of transactions enhances tax compliance and reduces the shadow economy.

Employment opportunities have expanded in fintech, app development, cybersecurity, and digital marketing. Startups have flourished, creating a vibrant ecosystem that drives innovation and job creation. The societal impact is equally significant: citizens experience greater financial empowerment, convenience, and participation in the broader economy.

Behavioral and Psychological Insights

Behavioral economics explains why individuals and businesses adopt digital payments. Convenience, reduced cognitive load, incentives, and social proof drive adoption. Merchants benefit from faster settlements, reduced theft risk, and easier bookkeeping. Over time, these behavioral reinforcements accelerate the replacement of cash, creating a self-reinforcing ecosystem of digital transactions.

Global Comparisons

India’s digital payment growth rivals that of China, where platforms like Alipay and WeChat Pay dominate. However, India’s interoperable system, supported by UPI, allows a decentralized approach that encourages competition and innovation. Lessons from other countries underscore the importance of infrastructure, trust, and regulatory support in achieving widespread adoption.

Future Outlook

The future of digital payments in India is poised for further expansion. Emerging technologies like blockchain, AI, and IoT are expected to enhance security, efficiency, and accessibility. Government initiatives will continue to promote financial inclusion, while fintech startups innovate new services and business models. By 2030, India may achieve a near-cashless economy, with digital payments becoming the primary mode for transactions across sectors.

FAQ

Q1: How significant is UPI in India’s digital payments ecosystem?

A1: UPI is central, processing over 20 billion transactions monthly in 2025 and enabling real-time, secure, cost-effective payments across banks and apps.

Q2: What role does government policy play in promoting digital payments?

A2: Policies like Digital India, PMJDY, PMGDISHA, and GST incentivize adoption by enhancing infrastructure, financial literacy, and compliance mechanisms.

Q3: What challenges hinder digital payment adoption in rural areas?

A3: Connectivity issues, digital literacy gaps, and trust deficits are primary barriers, addressed through government programs and fintech innovation.

Q4: How do digital payments impact SMEs?

A4: Digital payments improve operational efficiency, cash flow, transparency, and customer satisfaction, enabling SMEs to scale effectively.

Q5: Are digital payments secure in India?

A5: Yes, digital payments in India are secured through multi-layer authentication, encryption, and RBI guidelines. Risk-based authentication, AI-driven monitoring, and biometric verification further enhance safety. Users are also educated on avoiding phishing and fraud attempts, making the ecosystem highly reliable.

Q6: How have festivals and special events influenced digital payments?

A6: Festivals like Diwali, Navratri, and wedding seasons see spikes in digital transactions due to convenience, cashback offers, and government incentives. In 2025, Navratri alone witnessed a near tenfold increase in UPI transactions in a single day, highlighting the behavioral shift from cash to digital.

Q7: How does India compare with other countries in digital payments adoption?

A7: India is among the fastest-growing digital payment markets globally. UPI’s interoperability is unique, unlike China’s Alipay or WeChat Pay, which are platform-specific. India’s approach encourages competition, innovation, and cross-bank usage, enabling broader inclusion.

Q8: What impact do digital payments have on the informal economy?

A8: Digital payments reduce the informal economy by formalizing transactions. They increase transparency, help track taxable revenue, and encourage regulatory compliance, ultimately boosting government revenues and economic efficiency.

Q9: How do fintech startups contribute to digital payment growth?

A9: Startups like PhonePe, Paytm, Razorpay, and BharatPe innovate with user-friendly apps, merchant solutions, and fintech services. They drive adoption by offering features like instant transfers, merchant lending, rewards programs, and education for digital literacy.

Q10: What is the future outlook for cashless India?

A10: By 2030, India is expected to approach a near-cashless economy, with most transactions happening digitally. Emerging technologies such as blockchain, AI, and IoT will enhance speed, efficiency, and security. Financial inclusion, continued government support, and behavioral adoption will further consolidate digital payments as the primary transaction method.

Conclusion

India’s transition from a cash-dominated economy to a digital-first financial system represents one of the most significant socio-economic shifts in its modern history. The rise of digital payments, spearheaded by UPI and supported by government policies, fintech innovation, and consumer adaptation, has fundamentally changed how Indians transact.

The decline of cash is not merely a statistical trend; it signifies an economic transformation that brings financial inclusion, efficiency, transparency, and convenience to citizens and businesses alike. SMEs and large corporations benefit from faster settlements, better accounting, and increased customer satisfaction, while consumers enjoy security, instant payments, and seamless experiences. Challenges like cybersecurity, rural access, and digital literacy persist but are steadily being addressed through policy, technology, and education. The behavior of Indian consumers—driven by convenience, incentives, and trust—ensures that digital adoption continues to grow.

Looking ahead, India is set to lead the world in digital payments innovation. With emerging technologies, supportive policies, and a digitally literate population, cash will gradually become secondary, paving the way for a modern, inclusive, and efficient financial ecosystem. India’s journey is not just about payments; it is about creating an empowered society where money flows seamlessly, securely, and digitally.

#DigitalPayments #CashlessIndia #UPI #Fintech #FinancialInclusion #DigitalIndia #UPI2025 #SmartPayments #EconomicGrowth #TechInnovation #MobilePayments #FutureOfFinance #FinancialLiteracy #DoYouKnow

Knowledge

Empowering minds with reliable educational content daily.

Newsletter Signup

© 2025 DoYouKnow. All rights reserved.

Stay Ahead of the Trends – Join Our Newsletter