Do You Know How Biometric Payments & Aadhaar-UPI Devices Are Powering India’s Digital Inclusion Revolution

Biometric payments and Aadhaar-UPI devices are reshaping India’s digital inclusion. Discover how this innovation empowers millions.

TECH & SCIENCE

Do You Know Team

9/21/20254 min read

Digital payments in India have transformed dramatically in just over a decade. What began with debit cards and internet banking has now expanded into one of the most sophisticated, inclusive, and scalable financial ecosystems in the world. The Aadhaar-UPI integration, paired with biometric payment devices, has emerged as a revolutionary development.

India, a nation with over 1.4 billion people, faced a daunting challenge: how do you bring rural citizens, daily wage workers, and those without smartphones or literacy into the digital economy? Traditional apps like Paytm, Google Pay, and PhonePe worked well in urban India. However, millions in villages and small towns lacked smartphones, steady internet, or even the confidence to type in a password.

This is where biometric payments linked to Aadhaar and UPI (Unified Payments Interface) step in. By merging the simplicity of biometric authentication (like fingerprint or iris scans) with the speed of UPI, India is making digital inclusion not just a goal but a lived reality.

1. The Genesis of Aadhaar and UPI

Aadhaar, launched in 2009, is the world’s largest biometric ID system, giving every Indian a unique identity number linked with fingerprints, iris scans, and demographic details. By 2016, UPI entered the scene, developed by the National Payments Corporation of India (NPCI).

When the two came together, it unlocked a system where your fingerprint became your wallet, and your Aadhaar number became your bank account address.

Imagine this: A woman in a village, who never owned a smartphone, walks to the nearest Aadhaar Enabled Payment System (AePS) device, places her thumb on a biometric scanner, and within seconds, receives or transfers money from her bank account. No passwords. No cards. Just her fingerprint.

2. What Exactly Are Aadhaar-UPI Biometric Devices?

Aadhaar-UPI biometric devices are essentially Point-of-Sale (PoS) machines or small handheld devices equipped with:

Fingerprint scanner / iris scanner

SIM card or internet connectivity

UPI-enabled payment software

These devices allow:

Cash withdrawals (Mini-ATM function)

Money transfers

Balance checks

Merchant payments

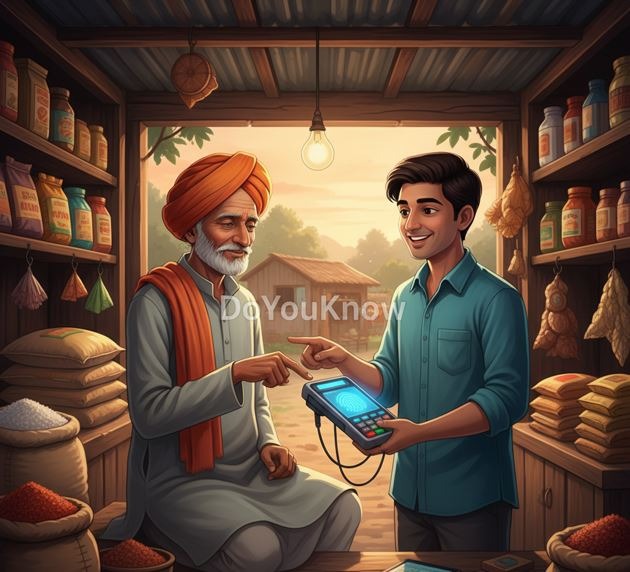

For example, at a village kirana store, a farmer can pay by simply placing his thumb on the scanner, authenticating via Aadhaar, and the money directly transfers through UPI to the merchant’s account.

3. Why Biometric Payments Are a Game-Changer for India

The magic lies in accessibility. India has over 65% of its population living in rural areas. A huge section of these citizens do not use smartphones or are semi-literate. Biometric payments solve this in multiple ways:

No smartphone required – just Aadhaar number + fingerprint.

No remembering PINs/passwords – biometric is enough.

Direct bank access – works with even basic Jan Dhan accounts.

Works in remote villages – through micro-ATMs carried by Business Correspondents (BCs).

This bridges the urban-rural digital divide, allowing digital inclusion at a scale never seen before.

4. Real-Life Examples and Impact

Take the case of Shradha, a vegetable vendor in rural Uttar Pradesh. She doesn’t own a smartphone. Previously, she only dealt in cash, often struggling with change. Today, she accepts payments via Aadhaar-UPI biometric devices. Customers pay her digitally, and her income directly reflects in her Jan Dhan account.

Or Ram Singh, a farmer in Madhya Pradesh. Instead of traveling 20 km to withdraw money from a bank branch, he now walks to his nearby ration shop, places his thumb on the biometric device, and withdraws cash instantly.

These real-world examples show how financial empowerment is touching the last mile.

5. Government and NPCI Initiatives

The Indian government and NPCI have been pushing biometric UPI payments aggressively. Key programs include:

AePS (Aadhaar Enabled Payment System)

BHIM Aadhaar Pay (launched by PM Narendra Modi in 2017)

Jan Dhan-Aadhaar-Mobile (JAM) Trinity for inclusive banking

Together, these ensure that every citizen, irrespective of their socio-economic background, gets equal access to digital finance.

6. The Technology Behind Biometric UPI Payments

Biometric devices function by connecting:

Biometric Data (fingerprint/iris) → Aadhaar Database (UIDAI servers)

Bank Account linked to Aadhaar → Validates customer identity

UPI Rail → Executes transaction instantly

Security layers include encrypted data transfer, UIDAI authentication, and NPCI’s UPI framework.

7. Challenges Ahead

While the system is groundbreaking, it faces hurdles:

Connectivity issues in remote villages

Device affordability for small merchants

Awareness gap among rural citizens

Concerns over biometric data privacy

However, with India’s digital push, cheap internet, and strong government willpower, these challenges are being steadily tackled.

8. The Future of Biometric Payments in India

Experts predict that biometric UPI devices could:

Replace cash transactions in rural markets by 2030

Expand into voice-enabled payments for illiterate users

Integrate with wearables and smartcards

Play a role in international remittances for migrant workers

Global fintech players are watching India closely, as this could become a blueprint for other developing nations.

FAQ

Q1: What is Aadhaar-UPI Biometric Payment?

It’s a system where citizens can use their Aadhaar-linked bank accounts and fingerprints/iris scans to make payments via UPI.

Q2: Can people without smartphones use biometric UPI devices?

Yes, biometric devices work without smartphones, making them ideal for rural and elderly populations.

Q3: How secure are biometric payments?

They use UIDAI’s Aadhaar authentication and UPI’s encrypted network, making them highly secure.

Q4: Are these devices available everywhere?

They are expanding rapidly through Business Correspondents, micro-ATMs, and Aadhaar-enabled merchant devices.

Q5: Can biometric UPI payments work offline?

Some devices allow offline authentication, though most require minimal connectivity.

Conclusion

The marriage of Aadhaar’s biometric identity system and UPI’s fast payment network is more than just a financial innovation—it is a social revolution. Biometric payments ensure that no Indian is left behind, regardless of whether they own a smartphone or not. It brings trust, transparency, and accessibility to the financial system, turning fingerprints into wallets and small rural shops into digital banks.

In essence, India is showing the world how true digital inclusion looks—where every thumbprint has the power to transact, and every citizen becomes part of the digital economy.

#DoYouKnow #DigitalIndia #AadhaarUPI #BiometricPayments #FinancialInclusion #UPI #DigitalRevolution #FintechIndia #RuralBanking #CashlessIndia

Knowledge

Empowering minds with reliable educational content daily.

Newsletter Signup

© 2025 DoYouKnow. All rights reserved.

Stay Ahead of the Trends – Join Our Newsletter